How much lending is too much? One could argue if the borrowing is affordable why shouldn’t the bank offer it? After all, we heard this argument hundreds of times, especially in 2020 and 2021 when interest rates were at their low. Banks were criticized, not just locally but internationally for being excessively harsh applying a stress test rate of nearly 6% at that time. Yet today if offered that rate it would be a bargain!

Since 2021, RBNZ has explored and held a public consultation on DTI restrictions. They’re now at their final round of consultation before a decision is made to introduce DTI and ease LVR restrictions.

Let’s take a look at the proposed changes and how this may affect your borrowing.

Implementing Debt-to-Income (DTI) Restrictions

What is it, and how is it calculated?

DTI limits the portion of lending that banks can provide to residential borrowers with a DTI ratio above a certain amount. It aims to reduce financial stability risks, support house price sustainability, and address gaps in existing policies.

It’s calculated by dividing the Total Debt by Total Annual Income, either individual or household.

The Proposed Changes & Affects

RBNZ is proposing to introduce DTIs to allow banks to lend:

- 20% of their residential loans to Owner-Occupiers with a DTI greater than 6, and;

- 20% of their residential loans to Investors with a DTI greater than 7.

It’s important to note, that this proposal would be aimed at only new lending applications, not existing ones. So, if your financial situation has changed and your DTI may be more than those numbers unless you’re making major changes to your lending, you’re unlikely to be impacted by this.

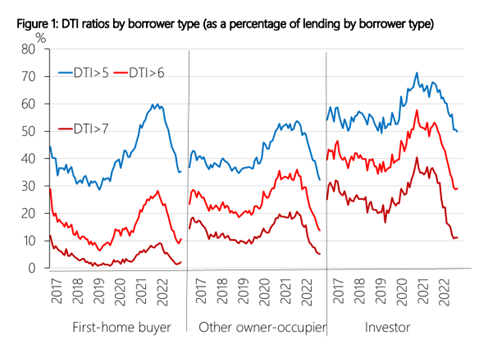

Debt-to-income ratio isn’t a new concept – they act as guardrails to prevent excess levels of borrowing. If these numbers were implemented today, they would make absolutely no difference to borrowing power. Banks are already heavily stress-testing, so most borrowers have a DTI between 4-6x, with an average of 5x in most instances. However, looking back in 2021 when interest rates were in the 2’s, banks were stress testing at 6% (and received significant criticism for being too conservative at the time!), but with rates being low, it wasn’t uncommon for owner occupiers to have DTI’s >6 and Investors >7. With these DTIs in place, this would limit some of those excess instances and act as a ‘guardrail’ preventing risky lending. See below, how almost 1/3 of borrowers had DTIs more than the proposed limits but it began to drop off quickly as interest rates began to rise.

Source: 09/11/2022 Framework for Debt-to-Income Restrictions – Regulatory Impact Assessment

Concerns with DTIs

The primary concern around the implementation of DTIs is the definition of Income. Currently, every bank has its approach to determine ‘usable’ income. Will the RBNZ set the lending policy now or will banks still have the agency to decide what they are comfortable to rely upon?

Fortunately, we have some insight into this. In the 09/11/2022 Framework for Debt-to-Income Restrictions – Design Elements and Exposure Draft document, the RBNZ suggests taking all forms of personal income into the picture and allowing banks to take their own approach to variable income. The 20% limit is substantial enough for banks to theoretically make some judgment calls where needed. If implemented this way, DTIs aren’t the troll under the bridge we should be worried about.

Easing the Loan-to-Value (LVR) Restriction at the same time as activating DTI

LVR has been the main tool to limit the amount that can be borrowed relative to the value of a property.

The Proposed Changes & Affects

RBNZ is proposing to ease the LVR limits, whilst also activating DTIs to allow banks to lend:

- Max. 20% limit for Owner-Occupiers with an LVR greater than 80% (or deposit less than 20%).Currently, the limit is set at 15% and it sets the availability banks can lend to borrowers with low deposits. This will provide more choices to First Home Buyers (around bank choice) as right now most banks are prioritising their existing clients to ensure they don’t break that limit. It also means getting a ‘pre-approval’ would be easier as some lenders wait until a borrower has a property conditionally bought or attending an auction. When the limit was set at 10%, there were genuine issues around even getting approval for a first home buyer, the easing to 15% meant that access was easier but at 20% this will provide more choice and hopefully more competition in this sector. Overall, this is a net positive change.

- Max. 5% limit for Investors with an LVR greater than 70% (or deposit less than 30%).From Summer 2022 through to Winter 2023 the property market across NZ declined approx. 20%. All homeowners were impacted by this; however, a question needs to be asked about how much of a deposit safety net Investors need after such a decline.The current LVR is proposed to be increased from 65% to 70%, which means more investors who can prove their affordability will be able to access funding. From our client base, I can tell that most investors are limited by their provable income rather than equity, however, first-time investors and investors who are making improvements to their properties need more equity so this would help that subset of investors the most. Again, a net positive change – and the risk is mitigated by the fact the market has already declined substantially since its peak.

What’s Next?

Consultation closes on Tuesday 12 March 2024 and I’ll be providing my comments. However, the more feedback they receive the better it is in the final implementation. Expecting to decide in the middle of 2024 with an implementation period beginning in 2025.

Our view is to apply DTIs as they’ve earlier proposed and let the banks have enough agency to make judgment calls. Taking this approach we’ll have a neat guardrail to prevent excess levels of borrowing and a more effective tool to control money creation and risk than the interest rate alone.

Overall, this is a positive revelation and it shows the RBNZ is actively looking at managing the downside risk of loosening the OCR (and therefore interest rates). We’re now asking the question of not ‘how high will interest rates go?’ but instead ‘how quickly will they fall?’. This year looks like a preparation period for the next season in 2025 and beyond. With DTIs in the picture, it can offer more stability to interest rate markets.

What do you think of RBNZ’s proposal to introduce DTI and ease LVR Restrictions?